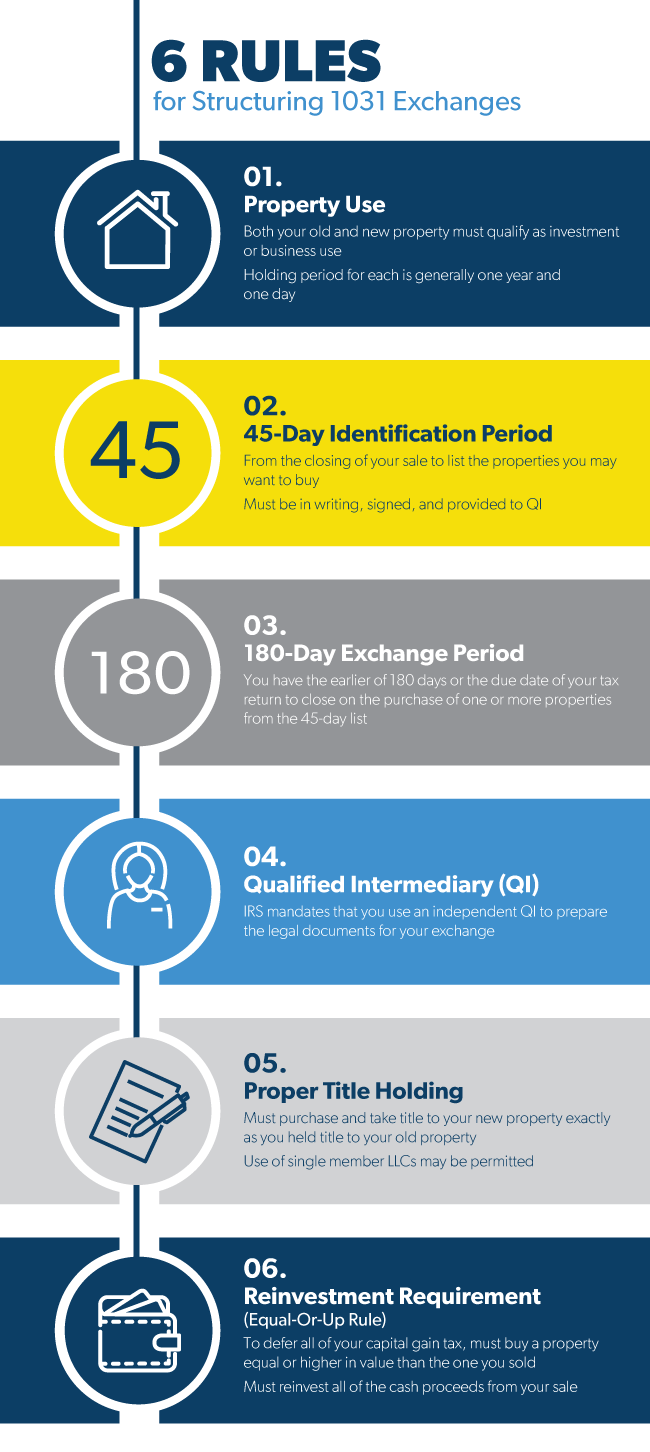

What property qualifies for a 1031 exchange?

Key Takeaways

- A 1031 property exchange allows you to defer (not eliminate) taxes on capital gains and the accumulated depreciation.

- Properties generally qualify for a 1031 exchange if they’re used in a business or for investment. ...

- You’ll qualify for a tax deferment only if you meet specific rules and timelines.

How often can I do a 1031 exchange?

A 1031 exchange involves the exchange of properties held for business or investment purposes. For capital gains taxes to be deferred, the properties being exchanged must be considered like-kind by the IRS. There is no limit to how many 1031 exchanges you can do or how often they can be done if done correctly.

What does not qualify for a 1031 exchange?

Personal property such as a primary residence, second home, or vacation home has never been eligible for a 1031 exchange. However, homeowners may qualify for up to $500,000 in capital gains tax relief on the sale of a residence if they meet the IRS’s home sale exclusion criteria. Are stocks or bonds eligible for a 1031 exchange? According to the IRS Fact Sheet on 1031 Exchanges, none of the following are considered “like-kind” for the purposes of a 1031 Exchange.

What is considered "like-kind" property for a 1031 exchange?

Generally, rental homes, condo buildings, and apartments are all like-kind, so are eligible for 1031 like-kind exchanges. Such property types are like-kind for two reasons. First, they generate income through lease and rental agreements. Second, they are not owned primarily for personal use.

How soon after a 1031 exchange can you sell?

1031 Exchange Timing and Deadlines Deadlines are crucial to 1031 exchanges. Investors must identify replacement properties for their relinquished assets within 45 days, and they must close on those properties within 180 days. Failure to meet either deadline could result in a disqualified exchange.

What is the three property rule in a 1031 exchange?

The Regulations allow identifying multiple properties. A Taxpayer may identify as many as 3 alternate properties of any value. If more than 3 properties are identified, the value of the 3 cannot exceed 200% of the value of the Relinquished Property unless 95% of the properties identified are acquired.

What disqualifies a property from being used in a 1031 exchange?

The property must be a business or investment property, which means that it can't be personal property. Your home won't qualify for a 1031 exchange. However, a single-family rental property that you own could be exchanged for commercial rental property.

What is the 200% rule 1031?

The 200% rule allows you to identify unlimited replacement properties as long as their cumulative value doesn't exceed 200% of the value of the property sold.

Can you identify more than 3 properties in a 1031 exchange?

The 95 percent rule says you can exceed three properties when identifying properties for a tax deferred 1031 exchange.

What is the 200% rule?

200% Rule. This rule says that the taxpayer can identify any number of replacement properties, as long as the total fair market value of what he identifies is not greater than 200% of the fair market value of what was sold as relinquished property.

Which of these is one of the three primary identification rules in a 1031 tax deferred exchange?

When identifying a replacement property in a 1031 exchange, you're allowed to use any one of the following identification rules: The Three Property Rule, under which you identify more than three properties regardless of their value; The 200 Percent Rule, under which you identify more than three properties, provided ...

Can you buy more than 3 properties in a 1031 exchange?

The third rule is that you can exceed three properties and you can exceed 200 percent of that relinquished property in value, but you have to close 95 percent of the aggregate value of all properties identified.